Planning for retirement is without a doubt a long-term, big picture endeavor. It takes decades of preparation and adjusting your plan to life’s changes to pull off successfully. Because we put so much into the preparation for retirement, many of us likely believe that we will retire exactly when and how it is laid out in our plan; however, in a new study conducted by Allianz Life, more than half of Americans retire earlier than expected for reasons outside their control.

This study suggests that the general perception about when and how retirement will start is skewed. Unforeseen events and circumstances can prompt pre-retirees to leave the workforce sooner than planned. What’s even more startling is that this data was collected before the COVID-19 pandemic hit the U.S., which means that the current economic and health crises sweeping the country could impact this number even more. With larger companies such as Boeing[i] offering voluntary buyouts and early retirement packages and unemployment at a record high[ii], the likelihood that more Americans will be retiring early is highly probable.

So how can individuals successfully deal with an early and unexpected retirement? One of the most important things to do is work through a plan with a trusted financial advisor who can guide you through the following considerations.

1. Evaluate the Different Exit Packages: The value and structure of retirement packages will vary from employer to employer and should be explored carefully. If you are being offered an early retirement package or buyout, you need to evaluate whether or not they are offering a fair and equitable option and consider the tax implications of the structure. You should also consider the reality that you risk getting laid off later down the road if the company is in jeopardy and you don’t exercise this option when it is presented.

If you are choosing to retire voluntarily, you’ll likely have a choice between different retirement structures such as taking more cash up front and receiving less per month or phasing out your retirement date where you will continue to work for your employer as you begin to collect your benefits.

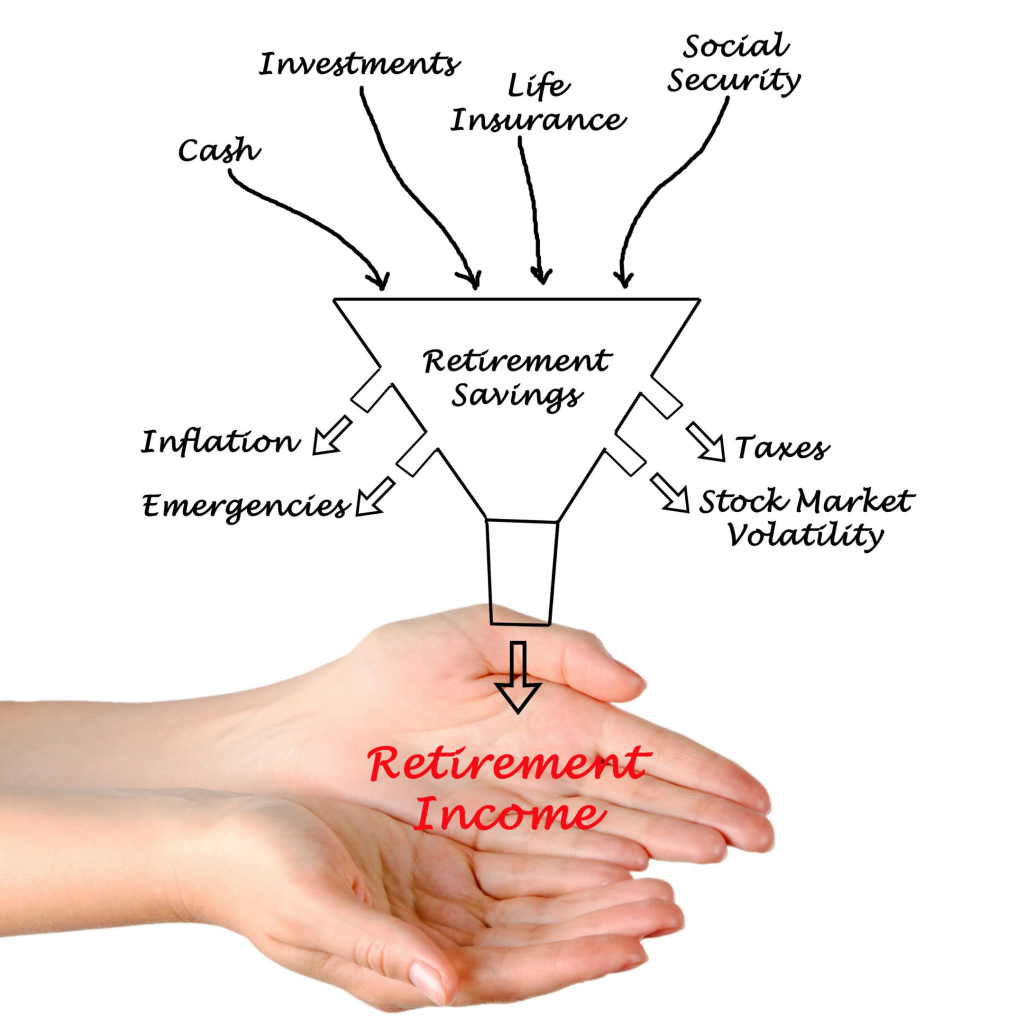

2. Align Your Exit Package with Income Planning: Of course, the decision about which package you choose should not be made in isolation, but in the context of your overall financial framework. You’ll need to factor in any other resources you have accumulated, when you will begin collecting social security, and how to best mitigate your tax burden amongst all retirement income sources. You should have a plan as to how you will craft your retirement paycheck. That is, how will you pool your income from each income source to cover your estimated living expenses? What does the longevity of that plan look like? Is it realistic, or do you need to adjust your drawdown in one or more areas to prepare for a long, secure retirement chapter?

3. Consider the Tax Implications of Each of Your Retirement Income Sources: As a high-income earner, the longevity of your retirement savings will partially depend on your ability to mitigate your tax burden in retirement. You will need to consider how each of your income sources will be taxed. Which funds will be tax-deferred, tax-free, and taxable? How will you account for that in your estimated retirement expenses? A prudent planning strategy is to generate income from each of these three “buckets” to help spread the tax liability out over time.

Furthermore, if you choose an early retirement plan that pays a larger lump sum at the beginning of retirement, how will you plan to receive it without bumping yourself into a higher tax bracket? You and your advisor may determine that a rollover would be appropriate and helpful in lessening your tax burden now and/or in the future.

4. Employee Stock Options: Choosing Between Exercising the Net Unrealized Appreciation (NUA) Rule or Performing a Rollover. In many publicly traded businesses, it is not unusual for companies to compensate employees with employer stock, granted through a profit-sharing plan or ESOP or by allowing employees to purchase shares within their 401(k) plans. Whenever company stocks are purchased within and withdrawn from a retirement account, they are not eligible to qualify for long-term capital gains rates and are taxed as ordinary income. However, the IRS offers a provision that allows for the more favorable long-term capital gains rate on the Net Unrealized Appreciation (NUA)[i] of employer stock after a qualifying event. But in order to exercise this option, the individual must report the cost basis of the stock in their immediate income taxes rather than deferring the tax burden for years or decades down the road. Therefore, individuals must evaluate which (if any) of theirthey plan to take in-kind (and when) and which they choose to rollover.

Putting a Flexible Plan in Place

While no one can predict what will happen with the COVID-19 pandemic or the economy, there are steps you can take now to help you prepare for the unexpected. The earlier you address your retirement income plans, the more likely you are to be positioned for retirement success—whether your retirement happens just as expected or comes earlier than planned.

If you are approaching or are in retirement and are worried about outliving your assets, the advisors at URS Advisory are here to help. We specialize in working with individuals and families who need personalized retirement guidance from a family-operated and family-oriented team that values your financial concerns. If you feel that URS Advisory could be a good fit for you, we invite you to schedule a complimentary, initial conversation with us to learn more about our services. We look forward to meeting you.

[i] Net unrealized appreciation (NUA) is the difference between the original cost basis and current market value of shares of employer stock.

[i] https://www.wsj.com/articles/boeing-to-offer-early-retirement-buyouts-as-coronavirus-takes-toll-11585798377?mod=searchresults&page=1&pos=1&adobe_mc=MCMID%3D21242702170232174992529127269747081245%7CMCAID%3D%7CMCORGID%3DCB68E4BA55144CAA0A4C98A5%2540AdobeOrg%7CTS%3D1595549280

[ii] https://tradingeconomics.com/united-states/unemployment-rate

Disclaimer: Advisory services are offered through URS Advisory LLC, a Registered Investment Advisor in the State of Florida. Insurance products and services are offered through URS Insurance, an affiliated company. URS Advisory LLC and URS Insurance are not affiliated with or endorsed by the Social Security Administration or any government agency. Investing involves risk including the potential for loss, and past performance is no indication of future results. Opinions expressed herein are solely those of URS Advisory. All written content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your financial adviser or qualified professional before making any financial decisions.